The brands will come and go. The infrastructure underneath them is where the real value is being built and SSMD Agrotech is positioning itself right at that layer.

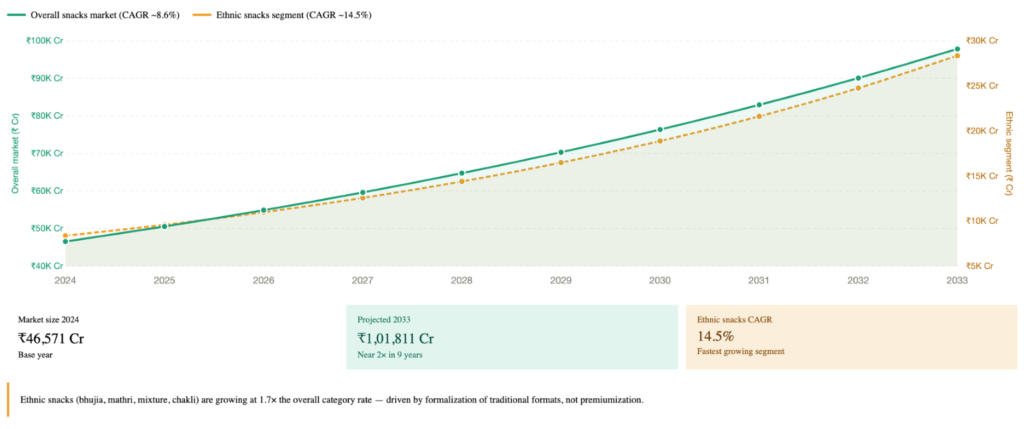

India is producing snack brands faster than it can sustain them. Dozens of D2C namkeen labels, ethnic snack startups, and regional FMCG plays have entered the market over the last four years, riding the same tailwind: India’s packaged snacks market at ₹46,571 crore in 2024, crossing ₹50,590 crore in 2025, and projected to reach ₹1,01,811 crore by 2033 at a CAGR of ~8.6%. The pitch decks write themselves.

But most of these brands will not survive the next three years. And that, counterintuitively, is where the most interesting investment opportunity in this sector actually lives.

The D2C Snack Graveyard Is Already Filling Up

Here’s the narrative the industry doesn’t want to say out loud: the D2C snack brand model in India is structurally fragile. Customer acquisition costs on Instagram and quick commerce platforms are rising faster than repeat purchase rates. Unit economics that looked attractive at ₹10–15 lakh monthly revenue collapse at scale. Distribution depth beyond metro pin codes remains elusive for most. Differentiation based on flavour or packaging alone has a shelf life measured in quarters, not years.

What this signals is a coming consolidation. The snack category won’t be won by the brand with the best Instagram grid — it will be won by whoever controls scalable, certified, cost-efficient manufacturing. The D2C wave is not the end game. It is the demand validation layer for the infrastructure play underneath it.

This is where companies like SSMD Agrotech, operating through the House of Manohar platform, a trusted name in agri-food processing since 1980, become strategically irreplaceable. When ten D2C snack brands fight for the same shelf space, and seven of them fold, the contract manufacturer who served all ten doesn’t just survive. It inherits the category intelligence, the optimised SKUs, and the production relationships. The graveyard is not a warning for SSMD. It is a pipeline.

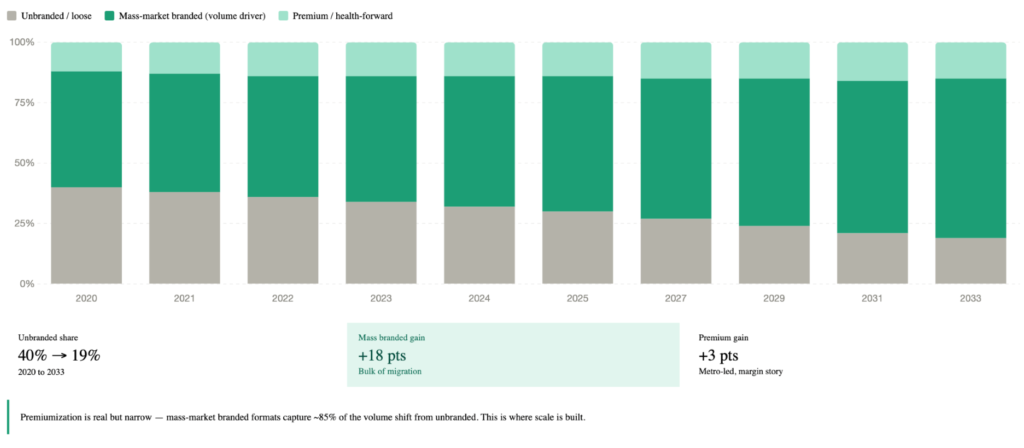

Premiumisation Is Real. But it’s a Metro story, and Metro is not the market.

The second narrative that needs challenging: the idea that India’s snack growth will be led by premium, clean-label, health-forward formats. It makes for elegant investor presentations. It is not where the volume is.

India’s snack consumption is a mass-market story. The real growth engine is a first-time branded buyer in Gorakhpur switching from loose namkeen at the corner store to a ₹10 packet she trusts because it has a recognisable label and a sealed pouch. That buyer is not counting macros. She wants hygiene, consistency, and value. Premiumisation in snacks is a metro mirage — the margin story, yes, but not the volume story. And in a market heading toward ₹1 lakh crore, volume is strategy.

General trade still controls ~50% of snack distribution nationally. Chips command ~42% of total market share, not because they are premium, but because they are accessible, consistent, and trusted. Ethnic snacks growing at a 14.5% CAGR are not growing because of artisanal positioning; they are growing because of formalisation: the movement of traditional recipes from unbranded loose formats into packaged, shelf-stable, trust-signalling products.

The real opportunity lies in building manufacturing infrastructure that can serve this mass-market formalisation at scale — not in chasing the premium tier that represents a fraction of total consumption.

The Infrastructure Layer That Outlasts Every Brand Cycle

SSMD Agrotech’s strategic positioning is not as a snack brand. It is the layer that makes snack brands possible — and that distinction matters enormously at this stage of market development.

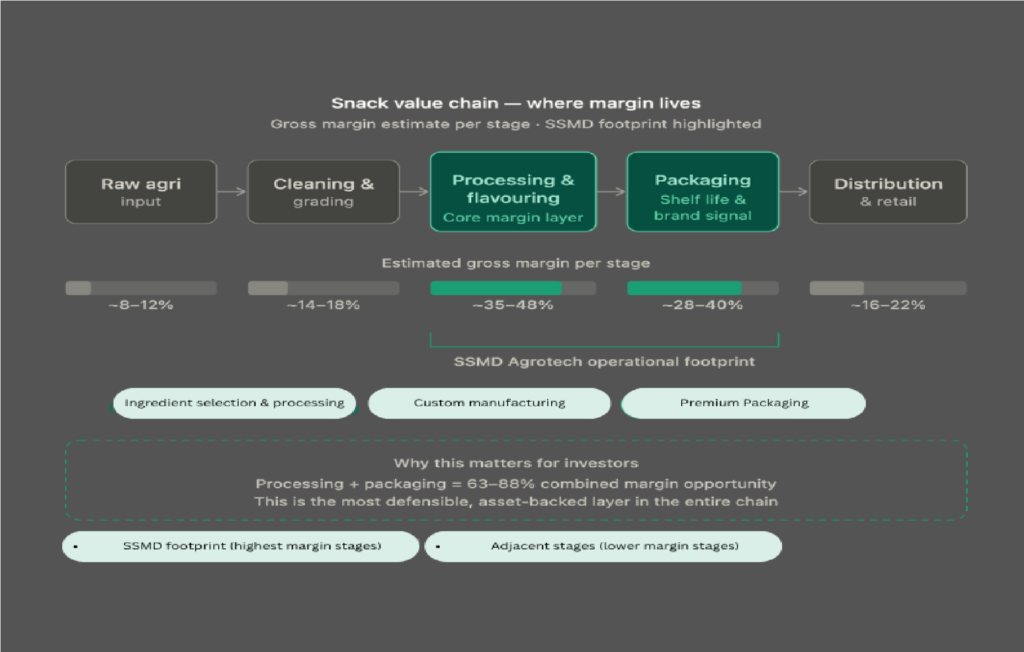

Its capability stack — advanced processing equipment; clean manufacturing facilities; custom manufacturing solutions; ingredient selection and processing; premium packaging; and a structured North India distribution network — maps directly onto what the next 500 branded snack entrants will need and cannot build themselves. The company’s “Dark Factory” concept for freshly processed daily essentials signals a forward-looking operations philosophy: automation-first, quality-consistent, and scalable.

For investors, the framing should be familiar: this is the picks-and-shovels play in a gold rush. When everyone is mining for snack market share, the defensible position is owning the shovel factory.

Four Strategic Vectors for Investors to Track

- Contract manufacturing at scale: As D2C brand consolidation accelerates, survivors will outsource manufacturing to reduce fixed costs. Certified, experienced partners with established supply chains will command premium contracts.

- Private label for quick commerce: Blinkit, Zepto, and Swiggy Instamart are building private label snack portfolios aggressively. They need reliable manufacturing partners, not brand equity.

- Mass-market ethnic snack formats: The 14.5% CAGR in ethnic snacks is a formalization story, not a premiumisation story. Standardised processing of bhujia, mathri, and mixture at volume is an underserved manufacturing niche.

- Export readiness: The Indian diaspora market across the UAE, the UK, and North America is actively seeking authentic, packaged ethnic snack formats. Processing standardisation and export-grade packaging are the qualifying criteria — not brand recognition.

India’s snack industry is not looking for its next Haldiram’s. It is looking for the company that makes the next hundred Haldiram’s possible.

SSMD Agrotech, with four decades of processing heritage, a scalable manufacturing infrastructure, and a platform already built for custom manufacturing and distribution, is positioning itself as exactly that — the farm-to-shelf infrastructure layer that a ₹1 lakh crore market will increasingly depend on, long after the D2C brand cycle has run its course.

The brands are the story. The infrastructure is the investment.

Naturally embedded keywords: India packaged snacks market, branded namkeen industry, agri-processing startups in India